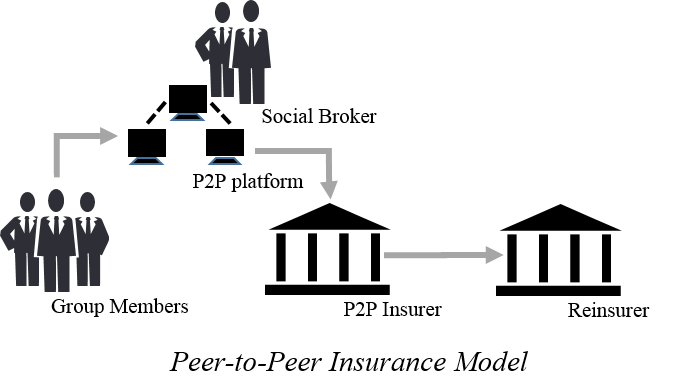

Peer-to-Peer (P2P) insurance is a risk sharing network where a group of individuals pool their premiums together to insure against a risk. Peer-to-Peer Insurance mitigates the conflict that inherently arises between a traditional insurer and a policyholder when an insurer keeps the premiums that it doesn’t pay out in claims. P2P insurance may also be referred to as "social insurance."

Breaking Down 'Peer-to-Peer (P2P) Insurance'

The demand for more accessible and low-cost services in the financial industry has brought about a number of technology-driven tools initiated by fintech companies. The insurance sector has not been left out of the technology drive that is changing the way consumers and companies relate with each other. Insurtech, technology innovation in insurance, has introduced tools for policyholders to have easy access to insurance coverage at lower costs than traditional policies allow. The incorporation of fintech concepts like the crowdsourcing platform and social networking led to the Peer-to-Peer (P2P) Insurance movement.

Peer-to-Peer (P2P) Insurance vs. Traditional Insurance

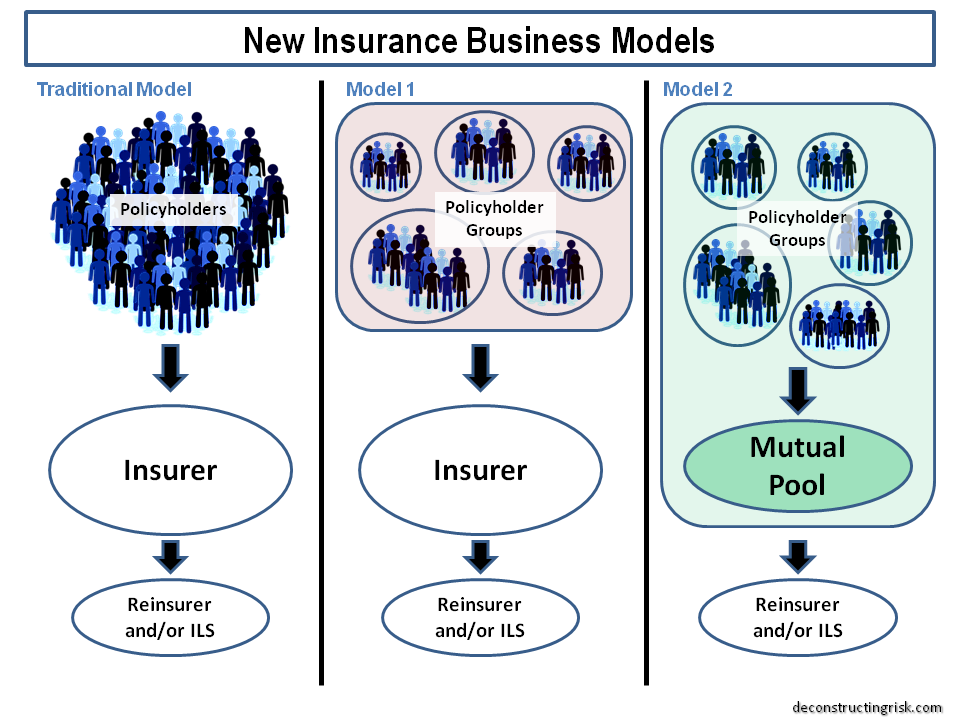

The traditional insurance model pools a large number of strangers under a similar coverage. An underwriter uses the profile information provided by each of these individuals to create a risk analysis of the individual. Information such as age, hobbies, and medical history are used to determine the premium that each policyholder would pay. The premium covers the cost of insuring the individual and provides assurance to the insured that in the event of a loss, s/he will be covered. The pool covers individuals with different risk profiles, with the low risk members paying less in premiums for the same type of coverage. In the event that one or more members or policyholders experience a catastrophic event, funds from the pool are used to cover the affected party(ies). The amount of excess in the pool at the end of the coverage period is retained by the insurance company as part of its revenue. Since most insurance companies are incentivized by profits, a conflict ensues between insurers and the insured when unused premiums are not refunded.

The P2P insurance model differs from the traditional model in a number of ways.

- The insurance pool is comprised of friends, family members, or individuals with similar interests who team up to contribute to each other’s losses. By selecting one’s pool members, the insured is assuming responsibility for the group’s risk profile. This selection technique would motivate an individual to initiate a pool that has a low risk outcome, and hence, low cost for the members. Also by pooling premium funds with known acquaintances, P2P insurance promotes transparency in its operations. Every member knows who is in the group, who is filing a claim, and how much money is in the pool. Finally, the P2P model solves the moral hazard associated with traditional insurance coverage. When members share the same affinity and know each other socially, there is a disincentive to file fraudulent or unnecessary claims.

- Any funds available in the pool when the coverage period ends are refunded to its members. This eliminates the issue that policyholders have with traditional insurers when both parties’ incentives are not aligned. Also, a P2P pool is insured by a reinsurer so when a group experiences claims in amounts that exceed the premium paid, the reinsurer covers the excess of available premium funds.

Peer-to-Peer (P2P) Insurance Pools

Different P2P insurance providers operate in different ways. Some pools only cover specific types of insurance such as auto insurance. Others require that members have similar causes like a support for ovarian cancer. Some groups even implement the crowdfunding tool to insure each other’s sick leave. Some providers refund unused premiums to the individual pool members. Others give the unclaimed premiums to a charitable organization or cause that unites the policyholders. A minute number of providers use Bitcoin as their currency of payment.

The innovative nature of P2P insurance has presented some challenges for insurance regulators who consider the P2P model different from the traditional one. Similar concerns across regulatory bodies that are seeing technology disrupt the traditional norm in the financial industry have given rise to a new group of companies called Regtech. Regtech uses innovative technology to help companies and industries partaking in digital advancements efficiently comply with industry regulators.

Other InsuTech Business Cases